Hanwha Q CELLS Co., Ltd. today reported its unaudited financial results for the three months ended June 30, 2015.

Highlights

- Total solar module shipments were 614MW, an increase of 12.2% quarter-over-quarter.

- Total shipments include 561MW of external shipments, 25MW of OEM and 28MW of shipments to the Company's own downstream projects.

- Net revenues were $338 million, an increase of 1.3% quarter-over-quarter.

- Average selling price (ASP) of external shipments was $0.59 for the quarter, no change from the previous quarter.

- Gross profit rose 20.7% quarter-over-quarter to US$58.4 million.

- Gross margin improved 277 basis points quarter-over-quarter to 17.3%, exceeding the Company's guidance of 15-to-17%.

- Total processing costs approached 42.5 cents per watt in June for in-house production.

- Cash balance rose to $476 million, an increase of 145%.

- Company generated $424 million in operating cash flow.

- The third quarter guidance is 800 to 820MW of total module shipments and gross margin should exceed 18%.

- The Company reiterates its FY2015 guidance of total module shipments of 3.2 to 3.4 GW and gross margin of 17 to 19 %.

Mr. Seong-woo Nam, Chairman and CEO of Hanwha Q CELLS commented, "The second quarter was the first full quarter reflecting the merger with Q CELLS in February of this year. In particular, shipment volumes were higher and growing, gross margins are expanding, our product quality is much improved, and our manufacturing scale and efficient production contributed to further reductions in our cost structure. Our ability to ship modules duty free to the US from plants in Malaysia and Korea greatly enhances our competitive position in that market, which now represents more than a third of our total shipments. We expect our US presence to improve further as we will begin to ship modules to NextEra to fulfill the 1.5 GW contract. Pricing remains higher in the US than other markets, so a bigger presence there will improve our profitability going forward."

Mr. Nam continued, "We remain on track to expand to 4.3 GW in both cell and module nameplate capacity by year end, making us one of the largest solar manufacturers in the world. Our fully-automated production facilities continue to enhance product quality and reduce costs. Our target of reaching fully optimized module manufacturing costs of low $0.40/W by year end is in sight and achievable."

"The company's downstream focus has begun to materialize with over 53MW of solar projects grid-connected in the U.K. during the quarter. We currently hold these projects on our balance sheet and we are in an advanced discussion with strategic buyers for the sales of these operating assets. We expect to sell approximately 150MW of operating assets in the U.K., Chile and Turkey during the 2H15. Project sales will be accretive to our earnings and will also provide additional liquidity near-term to assist in managing our financial leverage going forward."

Chairman Nam concluded by noting, "The outlook for the second half of 2015 remains robust. Visibility of orders is high and we will operate production facilities at full utilization in order to achieve our FY2015 shipment target of over 3.2 GW. ASP's should begin to stabilize for us, supported by a growing of our business in the US at healthier pricing. Our ability to further achieve benefits from the Q CELLS merger such as reduced operating expenses, supply chain synergies, and higher-quality, higher-efficiency products, all contribute to our confidence in achieving improved profitability for the remainder of this year."

Second Quater 2015 Results

Net Revenues

Total net revenues were US$338.0 million, an increase of 1.3%.

Total solar module shipments were 614MW, an increase of 12.2% quarter-over-quarter, which came in below our 2Q guidance due to certain shipments not delivered until early in the 3Q.

Total shipments include 561MW of external shipments, 25MW of OEM and 28MW of shipments to the Company's own downstream projects.

The average selling price (ASP) of external shipments remained unchanged at $0.59 quarter-over-quarter, largely driven by the sales increase in the US offsetting ASP declines in other markets, including certain emerging markets.

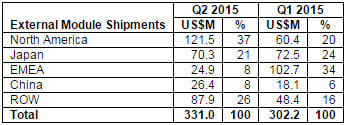

The table below reflects the geographic diversity of the Company's external module shipments in revenues. For the 2Q, North America became the largest market for the Company representing 37% of total shipments by revenue. Our ability to ship modules from Malaysia and Korea tariff-free into the U.S. has bolstered our competitive position. The Company maintained a healthy presence in Japan, one of the world's top three markets by volume, with 21% of its 2Q shipments going to that country. The EMEA region accounted for 8% of the Company's total shipments, much lower than the 34% total recorded during the 1Q15. This seasonal drop was largely contributed by significant pulled-in business during the 1Q in anticipation of EU's raising of Minimum Import Price. In addition, the UK, now Europe's largest solar market, was particularly strong ahead of incentive changes during the 1Q and paused during the 2Q to adjust to the new incentive structure. Although China will be one of the world's largest solar markets in 2015, we continue to take a cautious approach in view of lower pricing and credit risk. The Company expects to maintain shipments in China to 5-10% of total shipments for the remainder of the year. The rest of the world (ROW) accounted for a growing percentage of our shipments (26%) as the Company continues to penetrate new and growing markets, including India.

Gross Profit and Margin

Gross profit increased 20.7% to US$58.4 million from US$48.4 million in 1Q15. This increase in gross profit in 2Q15 was primarily due to further improvements in the company's cost structure.

Gross margin improved to 17.3% from 14.5% in 1Q15. The improved gross margin is the result of high utilization of manufacturing facilities and reduction in processing costs.

Total processing costs approached 42.5 cents per watt in June for our in-house production with little difference between using its own wafers and purchasing wafers. The Company's cost structure improved due to high utilization, improvements resulting from increased automation, and product lines that use fewer raw materials. The Company continues to benefit from the Malaysia facilities acquired from Q CELLS which manufactures cells at costs well below industry averages.

Operating Expense, Income and Margin

Operating profit was US$1.0 million, compared with an operating loss of US$17.3million in 1Q15.

Operating expenses were 17% of revenues. The company incurred higher upfront sales and marketing expenses during the quarter in anticipation of rapidly accelerating sales volumes in tandem with the manufacturing capacity ramp-up now underway. The company expects shipments in 2H15 to total 1.5 times those achieved during the 1H15, leading to a reduction in operating expenses as a percent of revenues to around 10% by year end. In addition, the Company expects the realization of reduction in redundant expenses associated with the Q CELLS merger to accelerate from the 3Q and onward.

Net Interest Expense

Net interest expense was US$14.8 million, compared with US$10.9 million in 1Q15.

Changes in Fair Value of Derivative Contracts

The Company recorded a net gain of US$1.2 million from the change in fair value of derivatives in hedging activities as compared to a net gain of US$8.2 million for the preceding quarter.

Income Tax Expense

Income tax expense was US$0.8 million as compared to income tax expense of $US2.3 million for the preceding quarter.

Net Income and Earnings per ADS

Net loss attributable to shareholders on a GAAP basis was US$14.2 million, compared with net loss of US$20.4million in 1Q15.

Net loss attributed to shareholders per share was US$0.00, compared with net loss per share of US$0.01 in 1Q15.

Net loss per basic ADS on a GAAP basis was US$0.17, compared with net loss per basic ADS of US$0.26 (retrospectively adjusted to reflect the current ADS to ordinary share ratio of one ADS to fifty ordinary shares effective on June 15, 2015) in 1Q15, on a 3.8% increase in average shares outstanding to 4,158,310,368

Financial Position

As of June 30, 2015, the Company had cash and cash equivalents of US$475.9 million. Total short-term bank borrowings (including the current portion of long-term bank borrowings) were US$456.5 million as of June 30, 2015. As of June 30, 2015, the Company had total long-term debt (net of current portion and long-term notes) of US$619 million. The Company's long-term bank borrowings are to be repaid in installments until their maturities, which range from one to three years. The Company's long-term notes are to be repaid within one year, and therefore the notes were classified as current liabilities as of June 30, 2015.

Net cash provided by operating activities in 2Q15 was US$423.5 million. As of June 30, 2015, accounts receivable were US$304.6 million. Day's sales outstanding ("DSO") were 83 days in 2Q15. As of June 30, 2015, inventories totaled US$444.6 million. Day's inventory was 138 days in 2Q15.

Capital expenditures were US$40.7 million in 2Q15.

Capacity Status

As of June 30, 2015, the Company had in-house production capacities of 1.3GW for ingot, 900MW for wafer, 3.4GW for cell and 2.1GW for module. The Company currently plans to expand its nameplate cell and module capacities to 4.3GW and 4.3GW respectively by the end of 2015. 600MW of the aforementioned new cell capacity is from the production facility operated by Hanwha Q CELLS Korea, an affiliate of Hanwha Q CELLS Co, Ltd.

Business Outlook

The Company provides the following guidance based on current operating trends and market conditions.

For the third quarter 2015, the Company expects:

- Module shipments of 800 to 820MW

- Gross margins of over 18 %

For the full year 2015, the Company expects:

- Module shipments of 3.2 to 3.4GW

- Gross margins of 17 to 19%

- Capital expenditures of US$280 million for cell and module capacity expansions and manufacturing technology upgrades; and up to US$110 million for PV downstream business.